Top Flexera Alternatives for FinOps & Cloud Cost Management

16 min read

Comparisons

Table of Contents

If you are evaluating Flexera One for FinOps and cloud cost management, the eight platforms worth looking at next are 1. Amnic, 2. IBM Apptio Cloudability, 3. Harness Cloud Cost Management, 4. PointFive, 5. Cloudchipr, 6. Finout, 7. CloudZero and 8. Vantage.

This guide sorts them by allocation depth, automation, Kubernetes coverage, AI cost coverage and pricing clarity. Scope note: the comparison is against the Flexera One FinOps and Cloud Cost Optimization modules (the former RightScale and Spot lineage), not the ITAM, SAM or SaaS-management modules in the same suite.

The best Flexera alternative tools:

Amnic: An AI-native FinOps platform that turns multi-cloud, Kubernetes and AI spend into allocation, automation and savings actions.

IBM Apptio Cloudability: Enterprise FinOps governance with deep chargeback, showback and reporting across hyperscalers.

Harness Cloud Cost Management: Engineering-led cost control with native Kubernetes AutoStopping and CI/CD integration.

PointFive: AI-driven deep waste detection across cloud, Kubernetes, Snowflake, Databricks and AI platforms.

Cloudchipr: Multi-cloud cost reporting with automation workflows and an Ask-AI assistant.

Finout: Shared-cost allocation, MegaBill and unit economics for finance-and-engineering co-ownership.

CloudZero: Cost per customer, per feature and per environment for SaaS unit economics.

Vantage: Fast multi-cloud and SaaS cost visibility with low setup time.

Why teams look for Flexera alternatives

Teams that started on Flexera (often inheriting it via the RightScale acquisition) typically reach a point where the buying centre shifts from central IT to a joint FinOps and engineering committee. At that point the pain list looks like this.

Opaque enterprise pricing with large annual minimums. Flexera does not publish FinOps-module pricing. An independent buyer guide puts the median Flexera contract near $24,000 per year and the observed maximum around $640,000 across 21 verified purchases, with custom-quoted multi-year contracts that lengthen evaluation against vendors that publish tiers. Based on May 2026 buyer-guide data.

Kubernetes cost lives in a separate module after the Spot acquisition. Flexera completed the Spot FinOps portfolio acquisition from NetApp in March 2025, so full Kubernetes cost coverage now sits in the Spot product line rather than the original Flexera One FinOps module. Teams that want a single allocated view across clouds, Kubernetes and AI spend typically end up running more than one Flexera console.

Limited anomaly detection and scheduled cost-spike alerting. Reviewers on a PeerSpot peer comparison of Flexera Cloud Cost Management call out weak anomaly workflows and slow drill-down on unexpected spikes.

Post-RightScale support and release cadence concerns. Long-standing customers on G2 reviews of Flexera One describe a slower release cadence and changing support contacts after the platform consolidation.

Dense UI and steep ramp for occasional users. The breadth of the suite (ITAM, SAM, FinOps, SaaS) shows up as a busy interface for FinOps practitioners who only need a slice of it.

Top Flexera alternatives: tools comparison

Platform | Best for | Multi-cloud and SaaS in one view | Allocation and unit economics | Optimization and automation | Kubernetes cost | Pricing model |

Amnic | All-round FinOps action across cloud, K8s and AI | Yes, AWS + Azure + GCP + SaaS | Yes, with virtual-tag-driven allocation and unit economics | AI-led recommendations with automated savings paths | Native, granular per-namespace and per-workload | Usage-based with a free audit; May 2026 data |

IBM Apptio Cloudability | Enterprise FinOps governance and chargeback | Yes, hyperscalers + custom data | Strong, mature chargeback and showback | Recommendations plus integration with IBM Turbonomic | Supported, less granular than K8s-native tools | Custom enterprise pricing; May 2026 data |

Harness Cloud Cost Management | Engineering-led automation | Yes, with CI/CD context | Cluster and service-level allocation | AutoStopping for idle resources, recommendations | Native, strong | Free tier, then usage-based; May 2026 data |

PointFive | AI-driven deep waste detection | Yes, AWS + Azure + GCP + AI platforms | Yes, with engineer-facing context | Agentic remediation, 400+ waste detections | Native, agentless | Custom pricing; May 2026 data |

Cloudchipr | Actionable multi-cloud workflows | Yes, AWS + Azure + GCP + SaaS data sources | Dynamic tag-based allocation | Scheduled automation workflows and Ask-AI | Supported | 14-day free trial, then tiered; May 2026 data |

Finout | Shared-cost allocation and unit economics | Yes, hyperscalers + SaaS via MegaBill | Strong, virtual-tag based | Recommendations focused | Supported | Custom enterprise pricing; May 2026 data |

CloudZero | Cost per customer or feature | Yes, hyperscalers + SaaS | Strong, code-driven allocation | Anomaly detection led, lighter on automation | Supported | Custom enterprise pricing; May 2026 data |

Vantage | Fast time-to-first-view | Yes, hyperscalers + SaaS connectors | Lightweight but quick to set up | Recommendations focused | Supported | Public tiered pricing with a free starter; May 2026 data |

How we evaluated these Flexera alternatives

Cost visibility scope. Does it cover AWS, Azure, GCP, Kubernetes, Snowflake, Databricks and AI platforms in one place.

Allocation model. How granularly can spend be split by team, service, customer, feature or environment, including untagged resources.

Automation depth. Does the platform stop at recommendations or does it execute actions (shutdowns, rightsizing, commitments).

AI cost coverage. Token spend, GPU spend, model-routing cost and inference cost as first-class views.

Pricing predictability. Public pricing or a known formula, with no surprise overage charges.

Time-to-first-insight. How quickly a new user can see allocated spend and a first savings recommendation after onboarding.

8 best Flexera alternatives

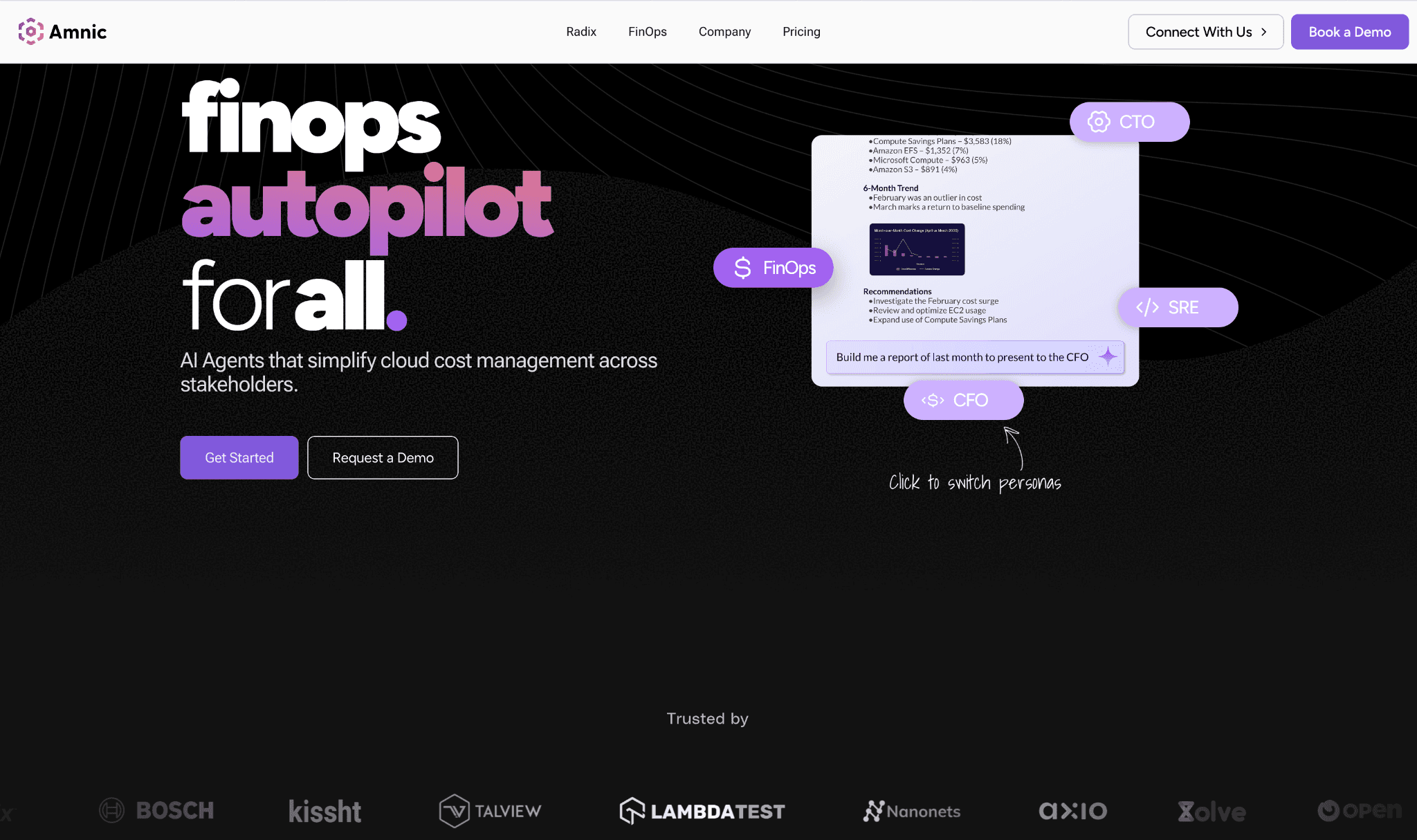

1. Amnic: Best overall Flexera alternative for FinOps action

Who gets benefited: FinOps and platform-engineering teams that want allocation, optimisation and AI-spend coverage in one place, with action rather than dashboards as the default behaviour.

Amnic describes itself as an AI-native FinOps platform that gives teams a single view of cloud, Kubernetes and AI spend, with continuous recommendations and automated savings paths. It is designed to be operated by a small FinOps team without forcing every engineer to learn a new console.

Why it is the strongest Flexera alternative:

Coverage spans the Flexera-One FinOps module plus the gaps Flexera customers usually outsource to a second tool: Kubernetes cost management and AI cost management.

Pricing is transparent and usage-based with a free audit, instead of a multi-year minimum.

The product is action-first: recommendations move into automated savings paths rather than sitting in a report.

What the platform actually lets you do:

See AWS, Azure, GCP and more platform spend in one allocated view, including untagged and shared resources.

Allocate Kubernetes cost down to namespace, workload and team without writing custom collectors.

Track AI cost (tokens, GPUs, inference, model routing) alongside cloud cost in the same allocation model.

Detect anomalies in near real time and route them to the right owner.

Apply rightsizing, idle-resource cleanup and commitment recommendations and watch realised savings accrue.

Set budgets, forecasts and chargeback rules that engineering and finance both trust.

Pricing model. Amnic offers a free audit and a usage-based subscription, with enterprise pricing on request, based on May 2026 data. See Amnic pricing.

Pros:

Single platform for cloud + Kubernetes + AI spend.

Action-first design: recommendations turn into automated savings.

Virtual-tag driven allocation closes the "untagged 20%" gap most FinOps teams live with.

Fast onboarding: a first allocated view inside a working day.

Transparent, usage-based pricing.

Cons:

Younger company than the established enterprise suites, so the partner and reseller footprint is smaller, per the vendor’s public company profile.

SaaS-management depth is intentionally outside scope; teams that need full SaaS-license governance will still pair with a dedicated SaaS-management tool.

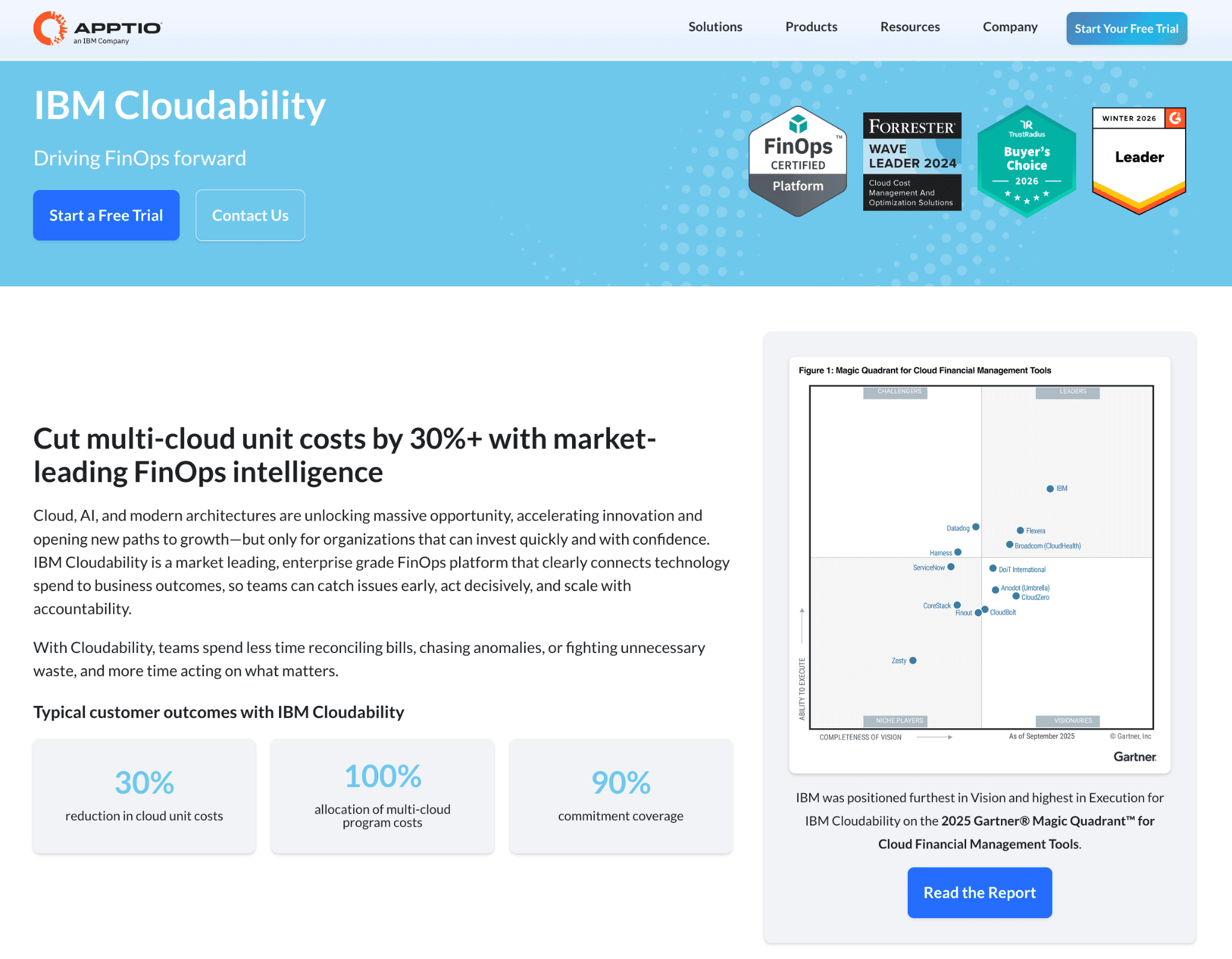

2. IBM Apptio Cloudability

Who gets benefited: Large enterprises that need standardised FinOps reporting, chargeback and showback across multiple hyperscalers, with a finance-grade audit trail and an existing relationship with IBM or Apptio.

Apptio Cloudability normalises cloud billing data into standardised reports and dashboards across AWS, Azure and Google Cloud, with a long-running focus on chargeback and showback for finance and IT leaders.

Ownership moved to IBM, as confirmed in an IBM Newsroom announcement of the Apptio acquisition, and the product now ships alongside IBM Turbonomic for automation and IBM Watson for AI-assisted analysis. For a focused view of where Cloudability falls short and which tools sit closest to it on a shortlist, see the Apptio Cloudability alternatives guide.

In practice:

Reporting and chargeback are mature and audit-friendly, with a finance-grade hierarchy of cost objects.

Optimisation actions usually require pairing with IBM Turbonomic, since Cloudability itself stops at recommendations.

Implementation typically runs through an IBM or partner-led engagement, with onboarding measured in weeks rather than days.

Coverage extends to AWS, Azure and GCP first-party billing, with newer support for SaaS-spend reporting via the wider Apptio suite.

Pricing model. Custom enterprise pricing quoted by IBM sales, with no public price list and minimum annual commitments, based on May 2026 data.

Pros:

Deep chargeback and showback maturity, including multi-level cost-object hierarchies.

Standardised cross-cloud reporting that maps cleanly to corporate cost-centre structures.

Strong fit when the company already runs ApptioOne for IT financial management.

IBM ownership brings procurement comfort for regulated enterprises.

Long history with Reserved Instance and Savings Plan recommendations across AWS and Azure.

Cons:

Pricing is not public, which lengthens evaluation, as reflected in buyer commentary on the PeerSpot Cloudability reviews page.

Native automation depth is lighter than Kubernetes-led tools; many customers add Turbonomic or a separate action layer for execution.

Onboarding is partner-led for most enterprise deployments, which slows time-to-first-insight versus self-serve platforms.

Kubernetes cost allocation, while supported, is less granular than tools built around Kubernetes from day one.

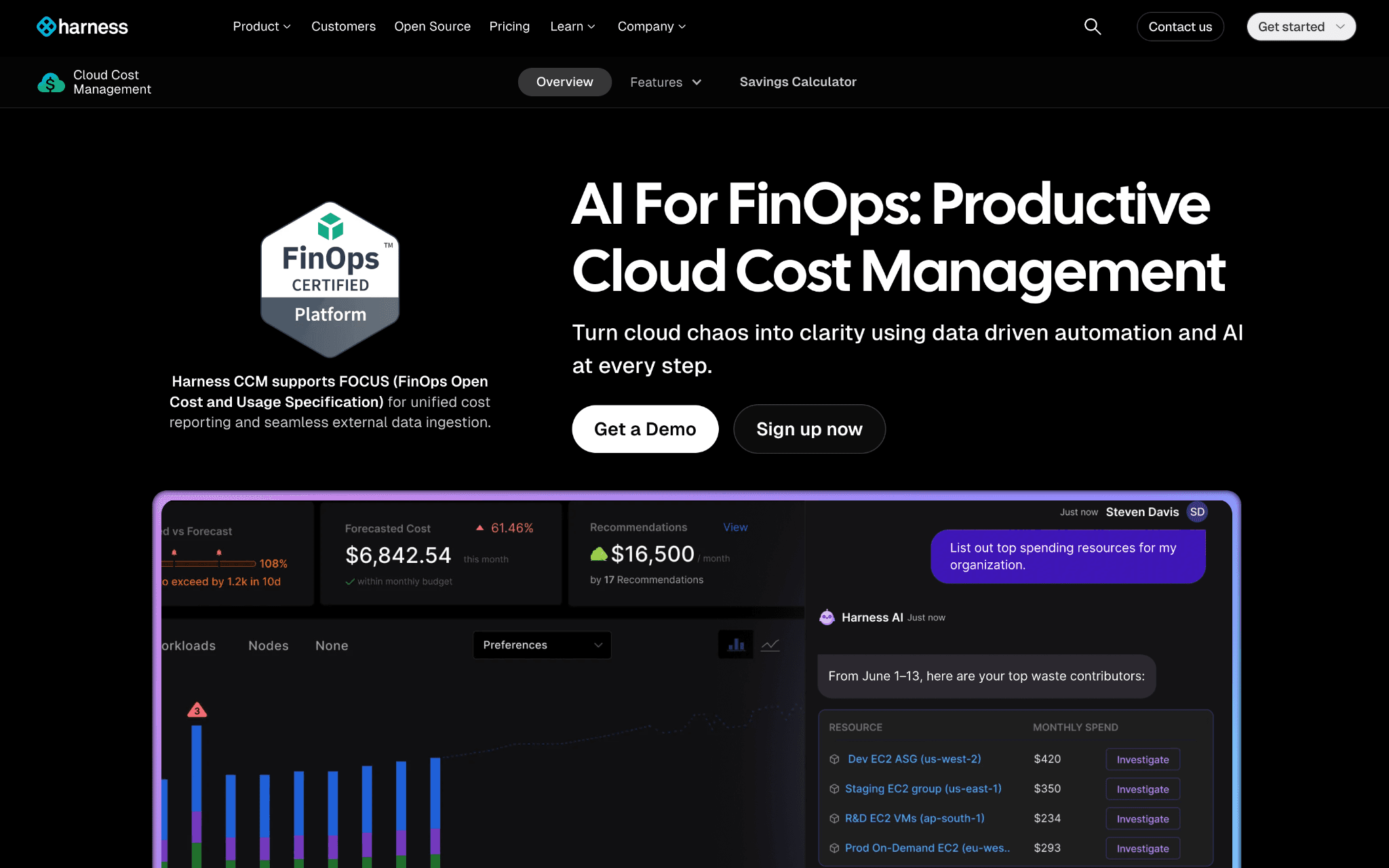

3. Harness Cloud Cost Management

Who gets benefited: Engineering-led organisations that want cost actions baked into CI/CD and Kubernetes, with the same control plane developers already use for delivery pipelines.

Harness Cloud Cost Management offers Cloud AutoStopping for idle non-production resources, granular Kubernetes cost visibility down to pod and workload, and a recommendations engine that flags rightsizing and commitment opportunities.

The product treats cloud cost as a software-delivery concern, which gives platform-engineering teams a single place to track delivery velocity and the dollars behind it.

In practice:

AutoStopping shuts down idle non-production workloads and brings them back on demand when a request hits the endpoint.

Kubernetes cost views are native and granular, with pod-level allocation that maps cleanly to teams and services.

Finance-side reporting and audit-grade chargeback are lighter than Cloudability or Finout, so finance-led teams often pair Harness CCM with a reporting layer.

The product sits inside the wider Harness software-delivery platform, which influences both the integration story and the commercial conversation.

Pricing model. A free tier covers smaller cloud footprints (publicly capped at a defined annual cloud spend), with usage-based paid tiers above that line, per the vendor’s pricing page, based on May 2026 data.

Pros:

Native Kubernetes cost coverage with pod and workload-level allocation.

AutoStopping is rare in this category and delivers measurable non-production savings.

Engineer-friendly because the cost view sits inside the same console as CI/CD.

A public free tier shortens procurement for smaller teams.

Recommendations cover rightsizing, idle resources and commitment opportunities.

Cons:

Finance-facing reporting and showback depth is lighter than dedicated FinOps suites, per the vendor’s own positioning.

Best value emerges when the wider Harness platform is in use, which expands the buying conversation.

AI cost coverage is less developed than vendors that have prioritised token, GPU and inference spend.

Multi-cloud coverage is solid for AWS, Azure and GCP, but SaaS-spend connectors are not the focus.

4. PointFive

Who gets benefited: Mid-market and enterprise platform-engineering teams that want behavioural waste detection across cloud, Kubernetes and AI platforms, with engineer-facing context and agentic remediation.

PointFive runs a proprietary DeepWaste Detection engine that analyses how cloud resources are actually used, not just how they appear on a billing report. The platform combines 400+ waste detections with agentic remediation, with native coverage of AWS, Azure, GCP, Kubernetes, Snowflake, Databricks and AI platforms.

The pitch is that traditional cost reports surface the obvious rightsizing candidates while behavioural detection finds the rest.

In practice:

Detections go beyond rightsizing into behavioural patterns the billing report misses, including idle data-warehouse compute and inefficient model-serving paths.

Coverage stretches into AI cost and data-warehouse cost, not just IaaS, which is uncommon in this category.

The product is engineer-facing, so finance teams still need a parallel reporting layer for board-level chargeback.

A Cloud Efficiency Hub gives FinOps and engineering teams a shared view of detected waste, remediation status and accrued savings.

Pricing model. Custom pricing by request from the vendor, with a typical enterprise commercial structure and no public price list, based on May 2026 data.

Pros:

Wide detection surface covering IaaS, Kubernetes, data platforms and AI.

Agentless Kubernetes integration removes a common deployment blocker.

Engineer-facing language and workflows make adoption easier in platform teams.

Detection depth meaningfully exceeds basic rightsizing recommenders.

Cloud Efficiency Hub gives a single shared view across FinOps and engineering.

Cons:

Newer entrant compared with IBM-owned, Broadcom-owned and Thoma-Bravo-owned platforms, which surfaces in enterprise procurement.

Finance reporting is not the primary lens; a parallel reporting tool may still be required for showback.

Commitment management exists but is lighter than dedicated commitment-automation tools.

Pricing is not public, which slows procurement comparisons against vendors that publish tiers.

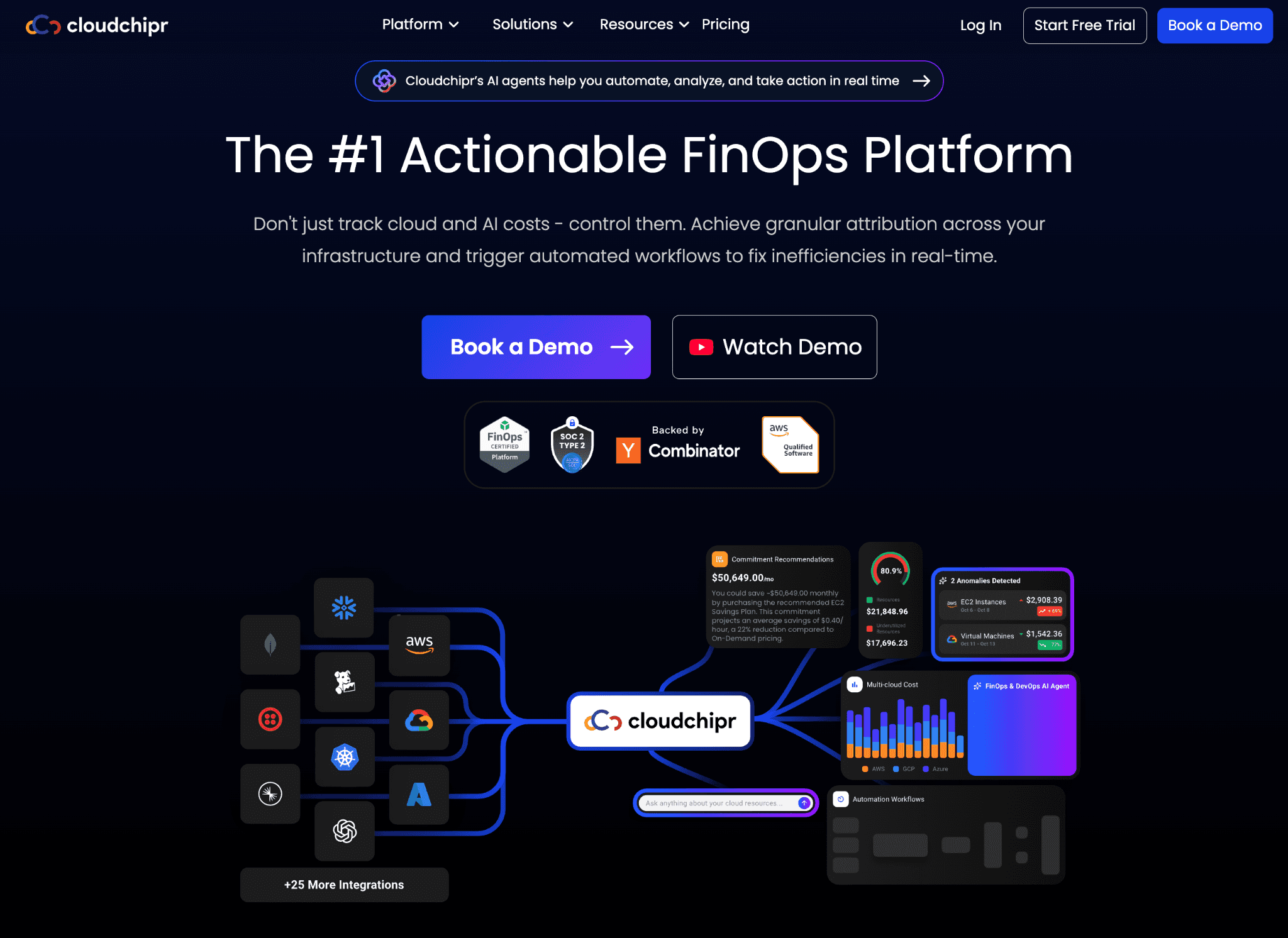

5. Cloudchipr

Who gets benefited: Lean multi-cloud FinOps teams that want cost reporting plus scheduled cleanup workflows without writing custom Lambda or Cloud Functions jobs.

Cloudchipr combines multi-cloud reporting across AWS, GCP, Azure, Kubernetes, Snowflake, Datadog and Confluent Kafka with automation workflows that shut down idle resources, resize underutilised instances and clean up stale snapshots on schedule.

An Ask-AI assistant answers cost questions in natural language, which lowers the bar for non-FinOps engineers who want to investigate a cost spike on their own.

In practice:

Automation workflows are the standout: cleanup and rightsizing run on a schedule or trigger, not on a Slack reminder.

Ask-AI gives engineers a quick path to “why did this go up” without learning a custom query language.

Onboarding is fast because reporting and action live in the same product and use the same identity model.

Coverage spans hyperscalers plus several data and observability platforms, which is broader than most reporting-only tools.

Pricing model. A 14-day free trial without credit-card capture, then tiered paid pricing per the vendor’s pricing page, with custom enterprise pricing at the top, based on May 2026 data.

Pros:

Strong automation-workflow library covering compute, storage and snapshots.

Multi-cloud and SaaS-data coverage in one console.

Ask-AI lowers the technical bar for cost investigations.

Public free trial removes a procurement step for evaluation.

Active release cadence backed by a Y-Combinator-backed product team.

Cons:

Finance-side reporting depth is lighter than Cloudability or Finout, per the vendor’s own positioning.

Larger enterprises often outgrow the workflow model and want a fully policy-managed action plane.

AI cost coverage is present but less developed than vendors that have made AI spend a first-class lens.

Allocation for shared infrastructure costs is lighter than virtual-tag specialists.

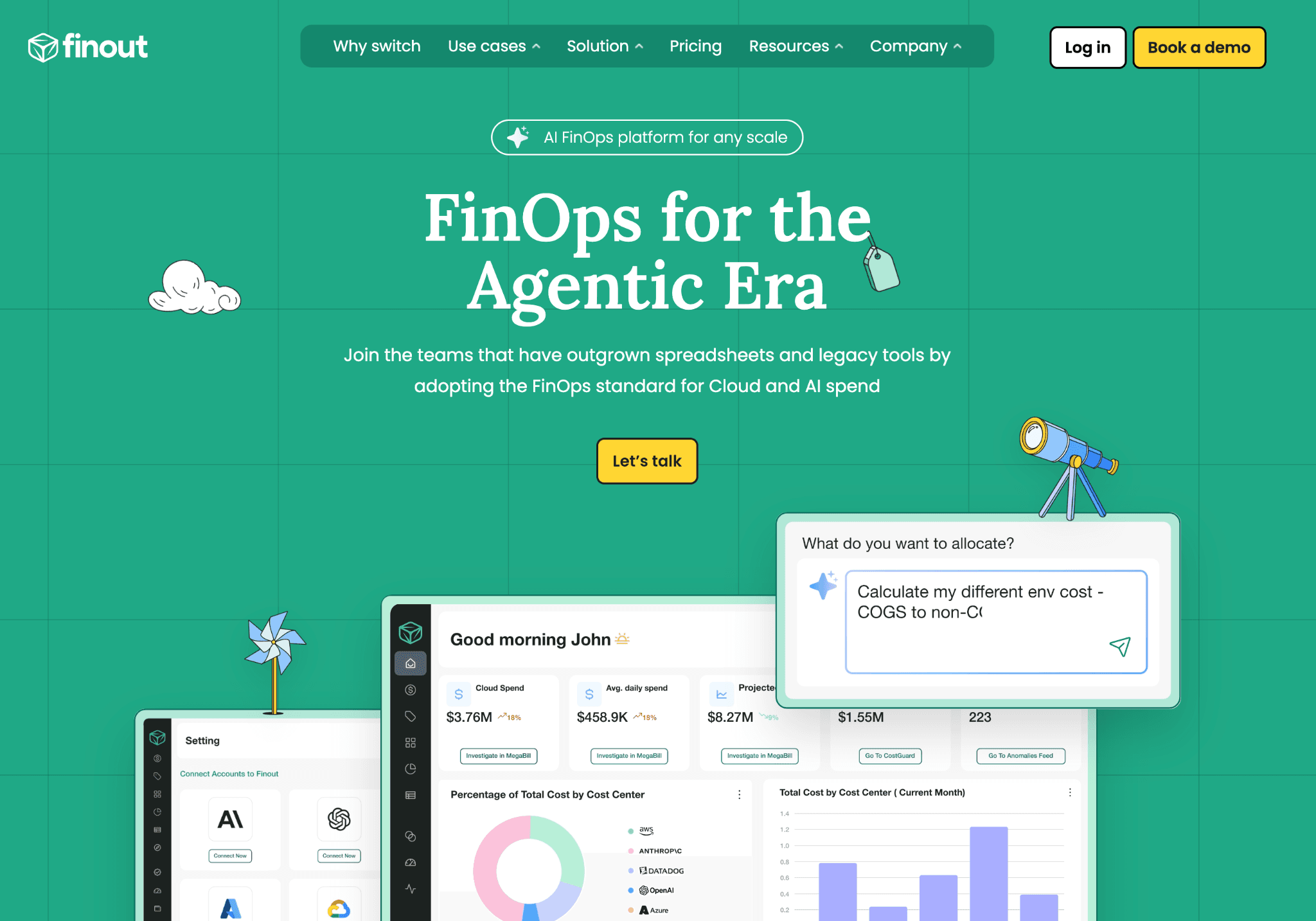

6. Finout

Who gets benefited: Finance-led FinOps practices that need shared-cost allocation, unit economics and a single virtual bill across cloud and SaaS spend.

Finout’s MegaBill aggregates cloud and SaaS spend into one allocation model, with strong virtual-tag support for shared infrastructure (Kubernetes shared services, observability platforms, data platforms) where native cloud tagging falls short.

The product is finance-leaning: reporting, allocation and CFO-readable views are the priority, with recommendations layered on top rather than at the centre.

In practice:

MegaBill is the differentiator for shared-cost allocation: one virtual bill that maps to teams, products and business units.

Virtual tags fix the “shared infra has no owner” problem most teams hit a year into their FinOps journey.

Action and automation depth is lighter than Cloudchipr or Harness, so this is typically a reporting and allocation choice with execution handled elsewhere.

Coverage spans AWS, Azure, GCP and a long list of SaaS data sources via direct connectors.

Pricing model. Custom enterprise pricing by request from the vendor, with no public price list, based on May 2026 data.

Pros:

Strongest shared-cost allocation in the category via virtual tags.

Clean single view across cloud and SaaS spend in one MegaBill.

Strong CFO-readable reporting that maps to corporate cost-centre hierarchies.

Mature anomaly detection with routing into ownership groups.

Good fit for businesses that need unit economics without heavy code instrumentation.

Cons:

Pricing is not public, which lengthens evaluation against tools that publish tiers.

Lighter on automated remediations; pair with an action-first tool for execution.

Kubernetes cost allocation, while supported, is less granular than Kubernetes-native tools.

AI cost coverage is present but less developed than vendors building AI-spend as a first-class lens.

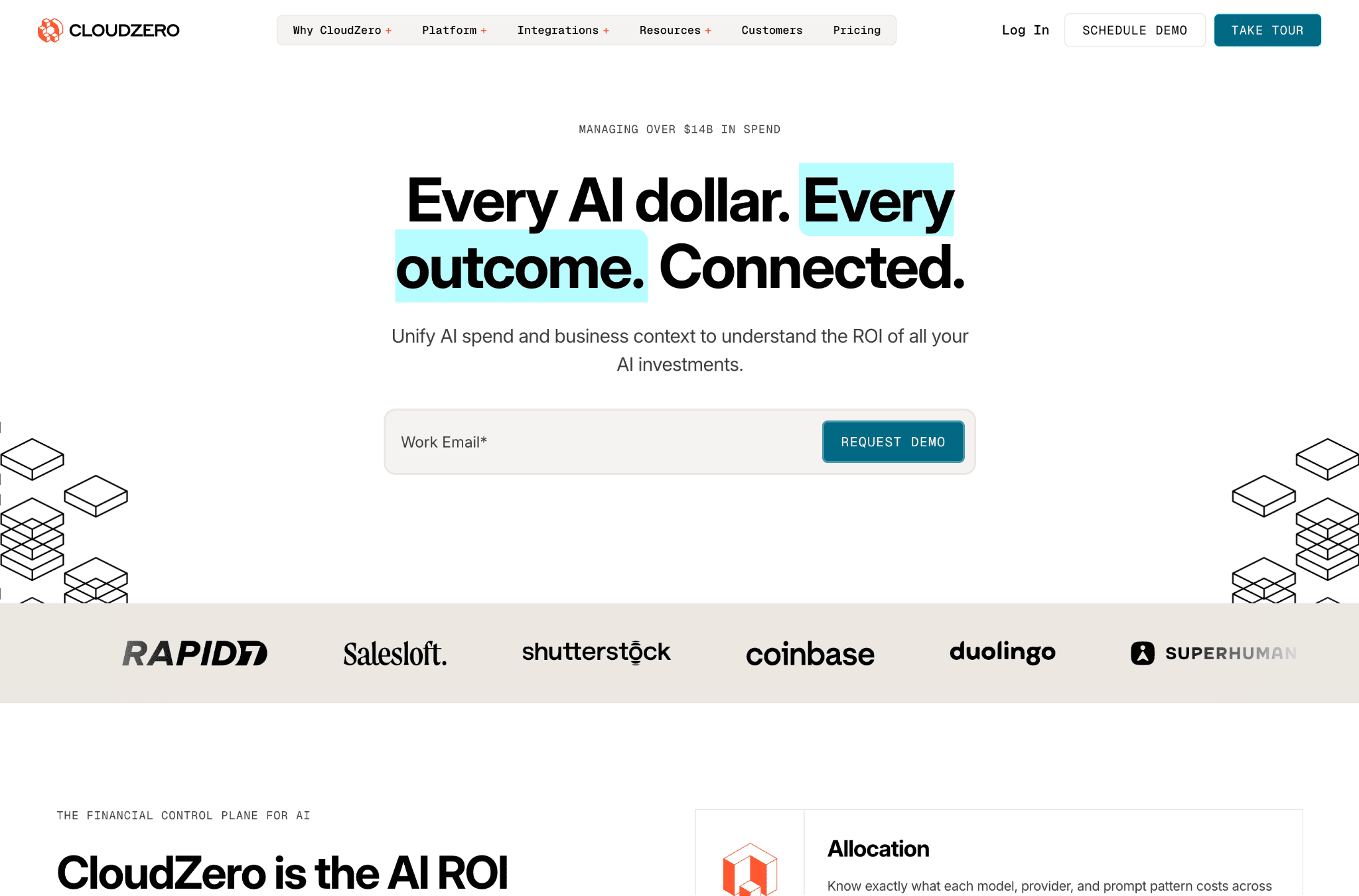

7. CloudZero

Who gets benefited: SaaS businesses that need cost per customer, cost per feature and cost per environment as the primary financial KPI, with engineering and finance owning the metric together.

CloudZero focuses on cost per unit (per customer, per feature, per deployment, per environment) with a code-driven allocation model that maps spend to business outcomes rather than only to infrastructure tags. The platform leans into measurement and anomaly detection rather than action and automation, which makes it a reporting and decision-support tool more than a remediation tool.

In practice:

Unit-economics views are the reason teams pick it, and they map cleanly to gross-margin-per-customer board metrics.

Allocation uses code-level and infrastructure metadata rather than relying only on cloud tags, which closes the untagged-cost gap.

Anomaly detection is mature, with team-level routing for cost spikes.

Action and automation are lighter than tools like Harness or Cloudchipr; CloudZero is the dashboard, not the action plane.

Pricing model. Custom enterprise pricing by request from the vendor, with no public price list, based on May 2026 data.

Pros:

Industry-grade unit-economics views, including per-customer and per-feature cost.

Strong anomaly detection with team-level routing.

Code-driven allocation closes the untagged-resource gap.

Clean fit for product-led SaaS finance reviews.

Cited as a board-reporting lens in several public SaaS-finance case studies on the vendor’s site.

Cons:

Pricing is not public, which slows evaluation against vendors with published tiers.

Native automation depth is lighter than action-first FinOps tools.

Kubernetes cost coverage is present but less granular than Kubernetes-native platforms.

AI cost coverage is less developed than vendors that have prioritised AI-spend allocation.

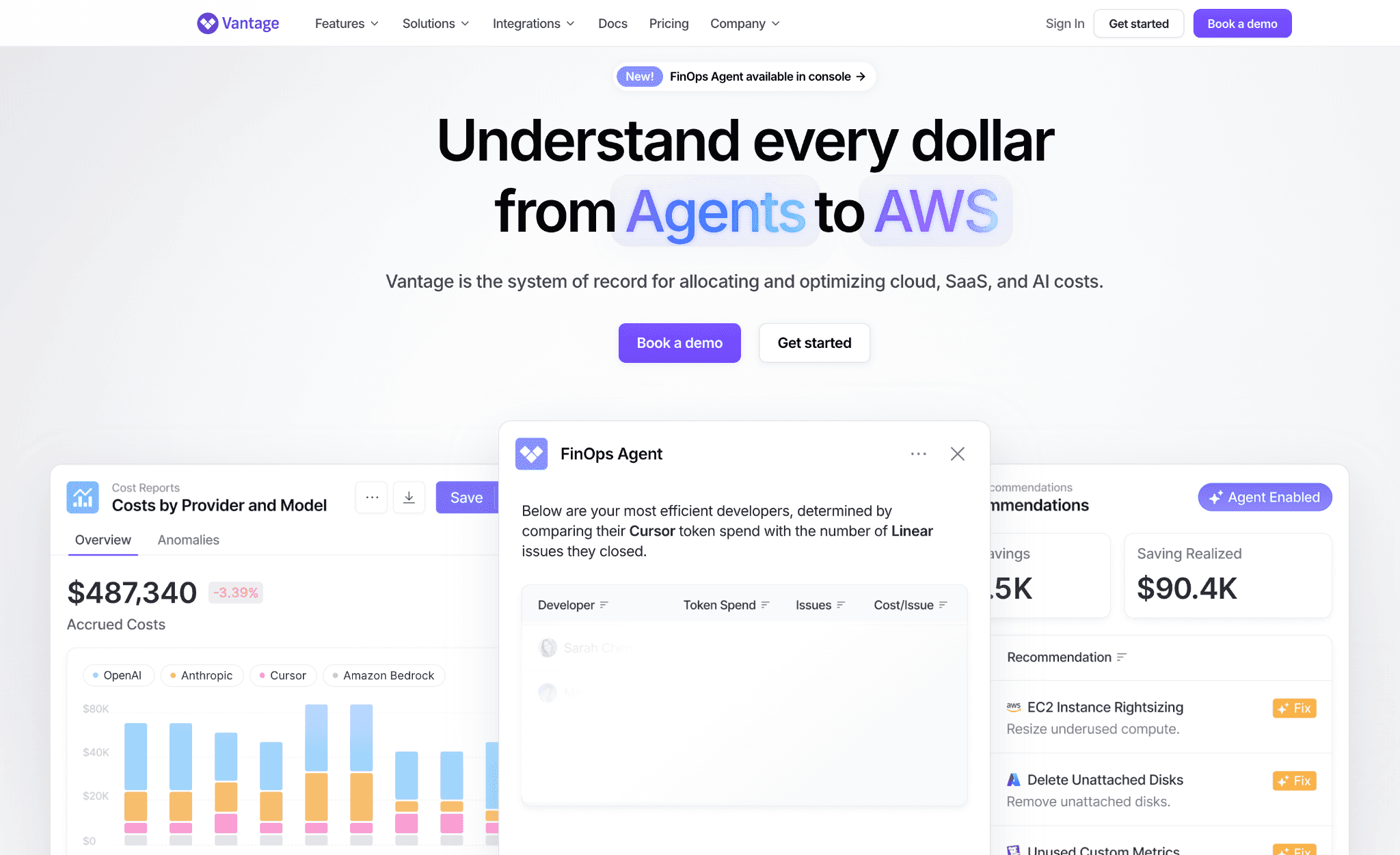

8. Vantage

Who gets benefited: Startups and mid-market teams that want a fast, low-friction cost view across cloud and SaaS, with public pricing and a self-serve starter plan that does not require sales contact.

Vantage offers connectors across AWS, Azure, GCP and a long list of SaaS tools, with a public tiered pricing model and a free starter plan. The pitch is time-to-first-view: a working multi-cloud cost dashboard inside a single working day, without an enterprise procurement cycle.

In practice:

A first allocated view shows up inside a day for most accounts, which is faster than the partner-led enterprise FinOps suites.

Coverage across SaaS connectors is wider than most peers, including observability, data and developer-tool spend.

Allocation and unit-economics depth is lighter than Finout or CloudZero, so larger teams often graduate from it as their FinOps maturity grows.

Public tiered pricing makes Vantage easy to slot into a credit-card-driven engineering budget.

Pricing model. Public tiered pricing with a free starter, per the vendor’s pricing page, based on May 2026 data.

Pros:

Public, tiered pricing with no sales contact required for the starter plan.

Wide SaaS connector list covering observability, data and developer tools.

Fast onboarding is measured in hours, not weeks.

Strong default dashboards that work out of the box.

Active community and changelog cadence.

Cons:

Allocation and shared-cost modelling are lighter than Finout, per the vendor’s own product comparison content.

Action and automation are not the primary lens; pair with another tool for remediation.

Kubernetes cost allocation is less granular than Kubernetes-native tools.

AI cost coverage is less developed than vendors building AI-spend as a first-class lens.

How to choose between Flexera and these alternatives

If you want focused FinOps, Kubernetes cost and AI cost in one product without bundling SAM, ITAM and SaaS-management into a multi-year suite contract, look at Amnic, Cloudchipr or PointFive.

If you are a cloud-native team that needs Kubernetes and AI spend in one allocated view, look at Amnic, PointFive or Harness Cloud Cost Management.

If finance needs chargeback and showback that engineers also adopt, look at Amnic, IBM Apptio Cloudability or Finout.

If the executive ask is unit economics per customer or per feature without heavy code instrumentation, look at Amnic, CloudZero or Finout.

If you want automated cleanup, rightsizing and commitment actions without writing scripts, look at Amnic, Cloudchipr or Harness Cloud Cost Management.

If shared-cost allocation across cloud and SaaS is the priority, look at Amnic, Finout or Vantage.

If the priority is the fastest possible first cost view across cloud, Kubernetes and AI in one console, look at Amnic, Vantage or Cloudchipr.

For a wider view of the category, see the top FinOps tools comparison and the cost allocation and unit economics tools roundup.

Frequently asked questions

What is Flexera?

Flexera is a software company owned by Thoma Bravo that sells Flexera One, a suite covering IT asset management, software asset management, SaaS management, FinOps and cloud cost optimization. The FinOps and cloud cost optimization modules trace back to the RightScale acquisition and the Spot FinOps portfolio acquired from NetApp.

What is the best Flexera alternative?

For FinOps and cloud cost management specifically, Amnic is the strongest all-round alternative because it covers cloud, Kubernetes and AI spend in one allocated view, ships action by default and prices transparently. The best fit still depends on whether the buyer is finance-led, engineering-led or product-led.

Why do teams switch from Flexera?

Common reasons include opaque enterprise pricing, thin native Kubernetes coverage in the FinOps module, limited cost-anomaly workflows and a heavier UI than a focused FinOps team usually needs. These themes recur across third-party review platforms and peer-comparison pages.

Is Flexera free or open-source?

No. Flexera One is a commercial enterprise platform with custom pricing and minimum annual commitments. There is no open-source edition.

How does Amnic compare to Flexera?

Amnic focuses specifically on FinOps and cloud cost action across cloud, Kubernetes and AI spend, with transparent usage-based pricing and a free audit. Flexera One is a broader suite that also covers SAM, ITAM and SaaS-management with custom enterprise contracts.

Does Amnic cover Kubernetes and AI spend?

Yes. Amnic provides native Kubernetes cost allocation down to namespace, workload and team, and tracks AI spend (tokens, GPUs, inference, model routing) alongside cloud cost in the same allocation model.

The category is shifting from visibility to action and from cloud to AI

The first generation of FinOps tools, the lineage Flexera bought via RightScale, was built to make cloud spend visible. Dashboards, tags and reports were the deliverable. That job is largely solved.

The second shift, happening across the rest of this list, is from visibility to action. Buyers no longer reward a tool for showing a number; they reward a tool for closing it. AutoStopping, agentic remediation, automated commitment management and virtual-tag-driven allocation are now the table stakes, not the optional add-ons.

The third shift is from cloud to AI. Token spend, GPU spend and inference cost are growing faster than IaaS spend in most engineering organisations, and the tools that started with cloud are the ones that need to extend first. Platforms that allocate AI cost in the same model as cloud cost will set the next baseline.

Better visibility and management into AI Tokens?

Start with a 30 day trial

Connect leading LLMs

24 hour time to value

Stay ahead of AI Spend

Make AI spend visible, controllable, and accountable.

Gain insights into your AI token costs at a team, customer, business unit and individual user level to measure and manage AI utilization.

Recommended Articles

Compare Input vs Output Token Pricing: Why Output Costs More and How to Budget for It

Read More

Vertex AI vs Bedrock: The Enterprise Platform Decision That Outlives the Token Price

Read More

Gemini vs GPT: Which AI Model Fits Your Workflow and Budget

Read More

H100 vs A100: Specs, Cost and Which GPU Wins for Your Workload

Read More

OpenCost vs Kubecost: Key Differences and How to Choose

Read More

6 Best Datadog Alternatives for Cloud Cost Management in 2026

Read More